*This article was first published on Healthcare Business Today on December 4, 2023*

The Retiree Drug Subsidy (RDS) is a government-funded program that has historically been the go-to choice for plan sponsors. Established under the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 (MMA), its simplicity, limited member impact, and convenience made it a reliable option that financially supported plan sponsors in providing prescription drug benefits to their retiree populations. However, the landscape has changed. Shifts in subsidies, changes within the pharmaceutical industry (biosimilars, gene therapies, lower cost generics), and adjustments to tax structures have diminished RDS’s financial advantages. Furthermore, with the Inflation Reduction Act of 2022, the case to move away from RDS becomes even more compelling. It’s time for employers to seriously consider a transition from RDS to an Insured Group Medicare Part D plan (EGWP) or a Medicare Advantage Part D plan.

The Inflation Reduction Act of 2022 was signed into law last August, establishing a diverse package of health, tax, and climate change provisions – including several provisions to lower prescription drug costs for Medicare patients and reduce federal drug spending. Implemented in phases, the first was designed to accomplish three things: capping out-of-pocket insulin prices at $35 a month, requiring rebates from drug companies if drug prices rise faster than inflation, and reducing adult vaccine costs while expanding coverage for them. Since RDS plans are commercial drug plans rather than Medicare plans, none of the price control measures enacted by the IRA will extend to RDS plans. Consequently, retirees on RDS plans will not benefit from the anticipated reductions in out-of-pocket costs.

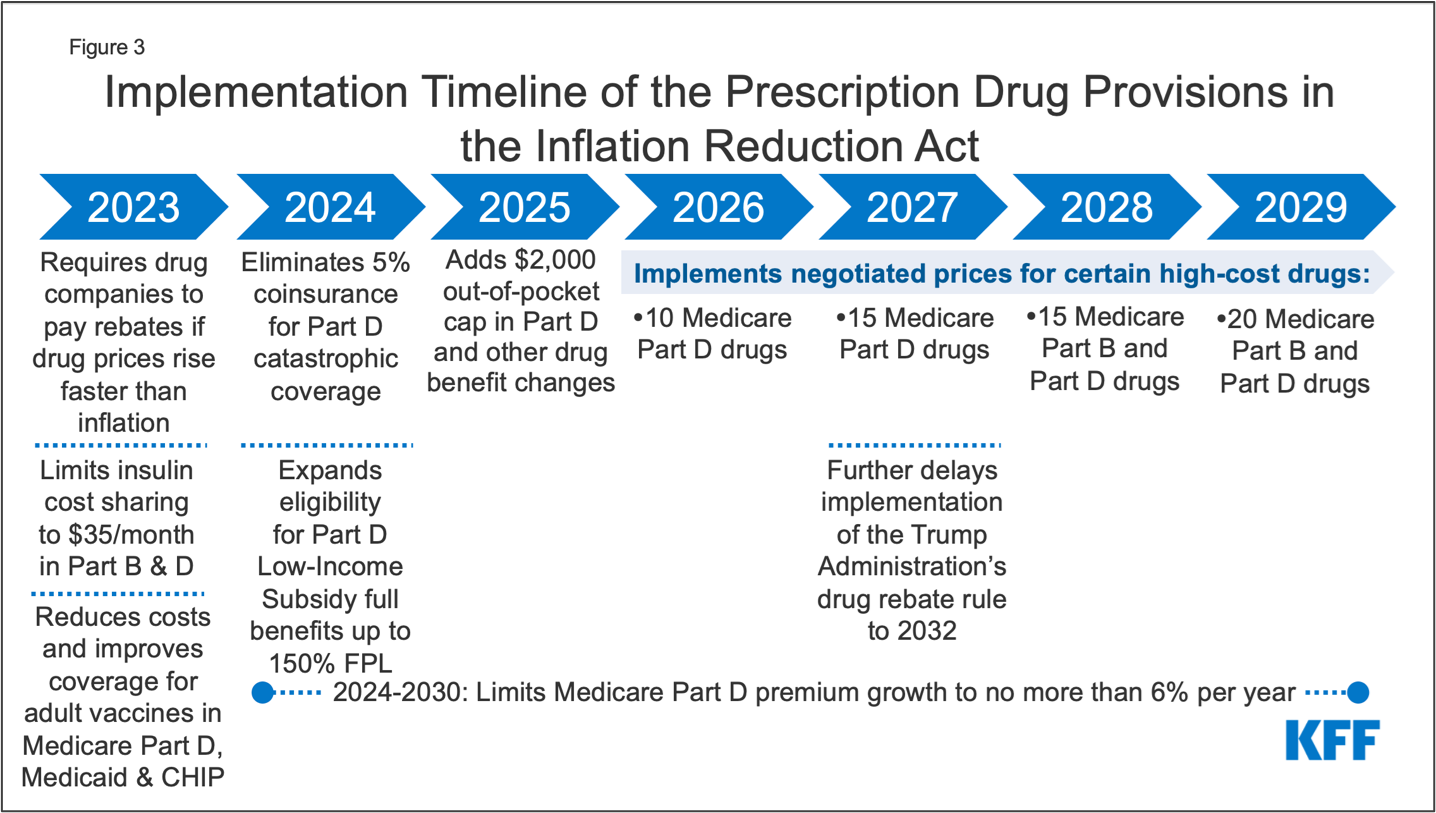

Another consideration is that RDS plans must be actuarially equivalent to the CMS basic plan which includes the member’s out-of-pocket costs being equal to, or less than, the CMS basic plan. The IRA enhances the CMS Part D basic plan, possibly making it more challenging to qualify for RDS subsidies. Due to the IRA changes in 2024, the member’s cost share will be reduced to $0 at the catastrophic coverage stage in the CMS basic plan. In 2025, the member’s out-of-pocket costs will be $2,000, which will significantly impact qualification for RDS. For reference, the following graph by the Kaiser Family Foundation illustrates the phases of the IRA.

Recent industry developments also underscore the urgency of transitioning away from RDS. Although the threshold and limit of drug costs qualifying for up to 28% subsidy increase each year, fewer people are landing in the 28% subsidy corridor. The declining cost of generics over time coupled with their increased use, means that fewer claims for individuals will fall into the 28% subsidy corridor. Additionally, the increased use of costly specialty medications and new and novel gene therapies are pushing claims for individuals outside of the 28% subsidy corridor.

Cost Threshold And Cost Limit By Plan Year

| Plan Year Ending | Cost Threshold | Cost Limit |

|---|---|---|

| 2022 | $480 | $9850 |

| 2023 | $505 | $10,350 |

| 2024 | $545 | $11,200 |

Source: https://www.rds.cms.hhs.gov/regulations-guidance/cost-threshold-and-cost-limit-plan-year

Moving from an RDS program to an EGWP might initially appear challenging. Plan sponsors may understandably have reservations about the considerable effort to transition their retiree population and potentially raise concerns over network changes, prior authorizations, and/or medication coverage. However, plan sponsors don’t have to navigate this transition alone. Retiree benefits management providers can ensure a seamless experience for both the employer and their retirees. Dedicated client and advocate teams can guide the process start to finish with continuity of care and educational outreach to retirees on their benefits, options, and available resources.

Given these significant changes and regulations in the healthcare landscape, transitioning to insured Group Medicare Part D plans is undeniably advantageous. For advisors who have clients on an RDS plan, we recommend a review of your clients’ plans to ensure eligibility and to discuss appropriate Medicare options (MA/MAPD, PDP, EGWP). With a fixed per-member-per-month structure, these plans cap the liability, providing greater predictability for healthcare expenses. This ensures cost savings, compliance, and financial stability for the employer’s budget, which can preserve their fund for generations to come. Now is the time for plan sponsors, brokers, and consultants to consider this strategic shift to drive material cost savings while improving the member experience with better care and outcomes for all.

*This article was first published on Healthcare Business Today on December 4, 2023*

Contact Us to Learn How RetireeFirst Can Help With Retiree Benefits Management at Your Organization