Group Medicare Advantage & Medicare Part D Prescription Drug Programs in 2025

Changes enacted by both the Centers for Medicare & Medicaid Services (CMS) and the Inflation Reduction Act (IRA) will significantly impact Medicare Advantage and Part D in 2025. These changes may affect plan sponsors’ costs and administrative and operational requirements. Understanding the changes, what they mean to retirees, and how to adapt is critical. The following is a use case on weathering change for clients as we all position to take on the future.

From the Medicare Modernization Act, Affordable Care Act, and now the IRA and changes from CMS: this is not the first shift to the Medicare landscape, and it won’t be the last. Change is inevitable. At RetireeFirst, our commitment to overcoming challenges for our clients and retirees is what defines us as a premier solution partner.

Charting the Path Forward in H1 2024: Navigating Changes from the Inflation Reduction Act & CMS

In the first half of the year, RetireeFirst helped our clients navigate headwinds by rapidly creating custom resources that curated and translated updates from CMS releases into vital, digestible information for group plan sponsors. After CMS released the Calendar Year (CY) 2025 Advance Notice for the Medicare Advantage (MA) and Medicare Part D Prescription Drug Programs and Draft CY2025 Part D Redesign Program on January 31, RetireeFirst crafted a summary brief for clients and presented an educational webinar open to the public. In our brief and webinar, RetireeFirst leaders outlined the MA and Part D payment and program changes that CMS was proposing to insurance carriers—and the potential impact they could have.

Our information also included the background and contributing impact of the IRA. The Inflation Reduction Act of 2022 is a law that continues to affect Medicare Part D prescription drug coverage now and into the future. The stated goal of the IRA was to make prescription drugs more affordable for retirees while reducing what the government contributes to the Medicare program. Less financial contribution from the government (CMS) and enrollees, will mean more contribution from drug manufacturers and Part D insurance carriers.

Hundreds of our webinar attendees were very engaged and submitted questions through our platform. We pulled their questions, and the steady stream coming in daily, into a growing Q&A document. Pooling a range of expertise—executive leadership, consultants, actuaries, and our partnerships with national carriers—we answered all questions in depth and circulated them internally. Our client-facing team members especially benefitted from the Q&A document as they fielded questions, prepared talking points, and conducted outreach so our clients would have the most time to prepare before the end of the year.

In the first week of April, CMS finalized their programs and payment methodologies for CY 2025 for Medicare Advantage and Part D. RetireeFirst reviewed the releases and finalized our resources with insights into the wider implications for group plan sponsors. These resources are available on our website and recommended for their educational content.

In this second of two informational webinars, we covered the following changes to MA/MA-PD and Part D plans in 2025 with visual aids and example scenarios.

Changes to Medicare Advantage Payment Methodology

- Updated Risk Adjustment Model

- Growth Rate Calculation

Changes to Medicare Part D

- Phases and Contributions Changes to the Standard Benefit

- $2k Annual Member Out-of-Pocket Spending Cap

- Potential Decrease in Risk Scores

- Medicare Prescription Payment Plan (M3P)

- Potential Impact on Retiree Drug Subsidy (RDS) Plans

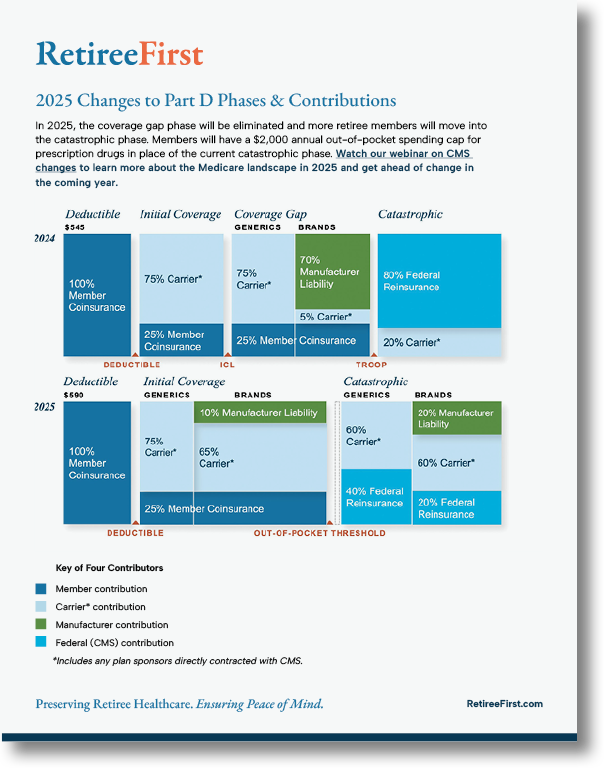

The financial contributions of the federal government, Medicare enrollees, Part D sponsors, and drug manufacturers will change next year. The coverage gap phase will be eliminated. Enrollees will have a $2k annual Part D prescription drug out-of-pocket threshold before they enter the catastrophic phase where they continue to pay $0, as they have since 2023. CMS will only contribute 40% of the cost for generic prescription drugs and 20% for brand-name drugs in the 2025 catastrophic phase compared to today’s 80% contribution for both drug types.

In turn, the insurance carriers will have to contribute 60% for both generic and brand-name prescription drugs compared to today’s 20% contribution for both drug types.

In our Part D Charts Comparison PDF, Color-coded blocks represent financial liabilities in the newly defined standard Part D benefit design. Calendar years are labeled on the left, and phases are grouped into labeled columns separated by thresholds that advance members from left to right into the next phase.

In addition to resources for group plan sponsors, we also created member-facing resources. As part of our Retiree Advocacy Services, we support clients with communications that educate their retiree members on plan-specific health benefits and opportunities to close gaps in care and improve wellness. This year, we also offered to create branded client letters communicating the IRA and CMS regulatory changes to members. Their purpose was to pare back the inherent complexity of Medicare regulations and create awareness about the drivers of change that could affect drug manufacturer costs, plan sponsor costs, and member premiums and benefits offerings. As with all member-facing materials, the language had to be legible and understandable to an elderly population. We use a Flesch Kincaid 8th-grade reading level and a large, 12-point font.

There’s still a lot of work to be done in the second half of 2024. However, our efforts have already paid off judging from positive survey responses using descriptions like “extremely informative, useful content” and “provided great context”. Some clients, like Tim Morrin, reached out to us directly to express their gratitude:

“I just wanted to thank the RetireeFirst team for organizing yesterday’s webinar. I thought it was essential, and gave me some ideas about how to game plan for the upcoming federal changes.”

Tim Morrin, Fund Administrator

Automatic Sprinkler Local 281, U.A. Welfare Fund

Medicare has always been complex, and advocating for retirees and improving their health outcomes have always been challenging. These are the very reasons our company exists. For almost 20 years, RetireeFirst has provided significant value to our clients, their benefits consultants, and their retiree members. Our track record stands at a staggering 99.9% client retention and 90+ Client NPS. In our most recent survey, 96% of members would recommend our Retiree Advocacy Services. Benchmark metrics prove that we’ve never let regulatory changes get in the way of our success.

Contact Us to See How RetireeFirst Can Help Your Organization